Markets Rebound Swiftly as Global Trends Shift

Market Recap for the Week of April 20, 2026

Markets are back at all-time highs. The recovery in stocks happened so quickly you could have missed it if you looked away for just a moment. This was a unique period for equities: they gradually drifted lower over the course of about two months, then surged in just two weeks, recovering all losses. Typically, we see the opposite during black swan events—sharp, rapid declines followed by a slower recovery.

Oil prices have remained elevated, around $95 per barrel, yet the stock market appears largely unfazed. This serves as an important reminder that stock returns are not strictly determined by economic fundamentals. We can experience a weakening economy alongside rising stock prices, and vice versa. Stock prices are ultimately driven by buyers and sellers who, for a variety of reasons, may be bullish or bearish at any given time. This is why using economic data to try to time markets in the short term is a fool’s game.

On a year-to-date basis, international developed stocks are ahead of U.S. stocks by about 1%, while emerging markets are significantly outperforming, with a 16.50% return compared to 5% for the S&P 500. Since January 1, 2025, both international segments have led the U.S., with developed markets outpacing by 16% and emerging markets by roughly 33%. The U.S. dollar is essentially flat for the year, making the strong performance of emerging markets particularly noteworthy. Any weakness in the dollar would likely provide an additional tailwind for international equities.

“Markets can recover just as quickly as they fall—often faster than investors expect.”

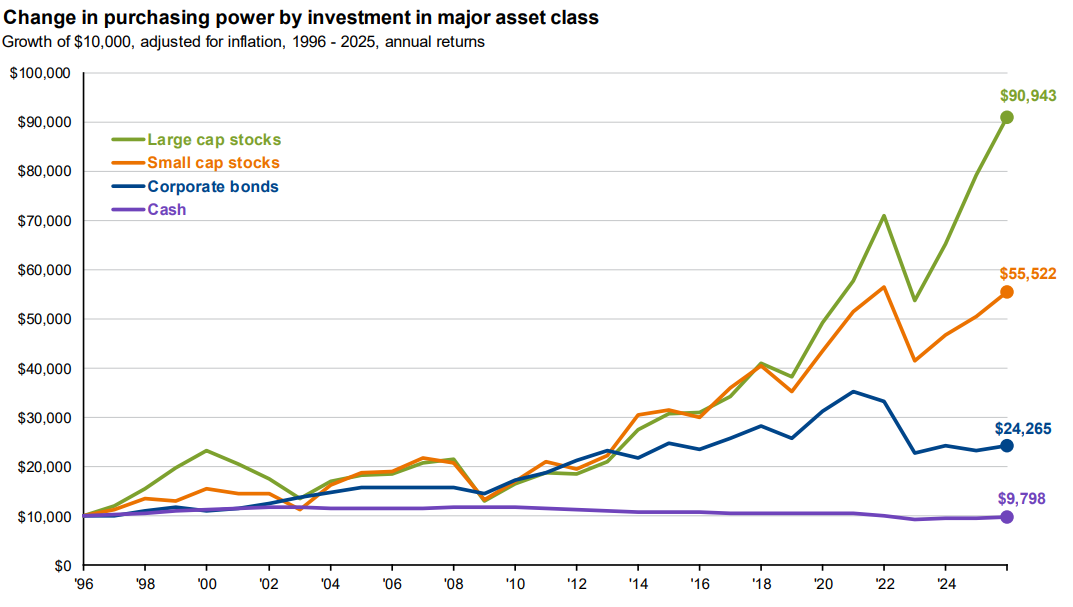

Chart of The Week

This week’s chart, sourced from the JPMorgan Guide to the Markets, illustrates the inflation-adjusted growth of various asset classes over a multi-decade period. The key takeaway is clear: cash significantly underperforms over the long term. For example, $10,000 held in cash for 30 years actually loses purchasing power and ends up worth less than its starting value. Importantly, this assumes the cash was invested in Treasury bills, which historically offer yields similar to high-yield savings accounts.

Even in a high-yield savings account, cash does little to build long-term wealth. While stocks and bonds may feel risky—and they can be over the short and medium term—the greater risk is often holding too much cash for too long. This is why maintaining a fully funded emergency fund while allocating excess cash to a diversified portfolio remains a prudent approach.

The commentary in this blog is for informational purposes only and should not be taken as personalized investment advice

Sources: Bloomberg, Bureau of Labor Statistics, Ibbotson, J.P. Morgan Asset Management. Large cap stocks: S&P 500 TR Index; Small cap stocks: Russell 2000 TR Index; Corporate bonds: Bloomberg Long U.S. Corporate Index; Cash: Bloomberg U.S. Treasury Bills Index. All returns are inflation-adjusted total returns, using annual average headline CPI inflation. Guide to the Markets – U.S. Data are as of March 30, 2026.