Markets Navigate Oil Shock Amid Rising Geopolitical Tensions

Market Recap for the Week of March 16, 2026

Nearly all major asset classes faced headwinds last week as the conflict in Iran continued to unfold. Oil prices remain elevated, hovering just below $100 per barrel. According to AAA, gasoline prices in California have risen by approximately $1.05 over the past month—an unwelcome development that adds renewed pressure to the inflation outlook.

Fixed income markets were not immune to the volatility. The 10-year Treasury yield moved higher throughout the week, resulting in declining bond prices. Within equities, performance has been uneven. Energy stocks continue to lead, with gains exceeding 30% year-to-date, while most other sectors are mixed—some modestly positive, others slightly negative. Financials have lagged the most, down over 10% on the year.

Somewhat surprisingly, the start of this year closely resembles the beginning of last year. In 2025, markets were pressured by tariff concerns; this year, the primary driver has been the sharp rise in oil prices stemming from geopolitical conflict. The key question now is whether markets will rebound as quickly as they did previously. While politics typically play a limited role in long-term market performance, policy decisions in the current environment may have a more immediate impact. A resolution to the conflict could help stabilize oil prices and, in turn, ease selling pressure across broader markets.

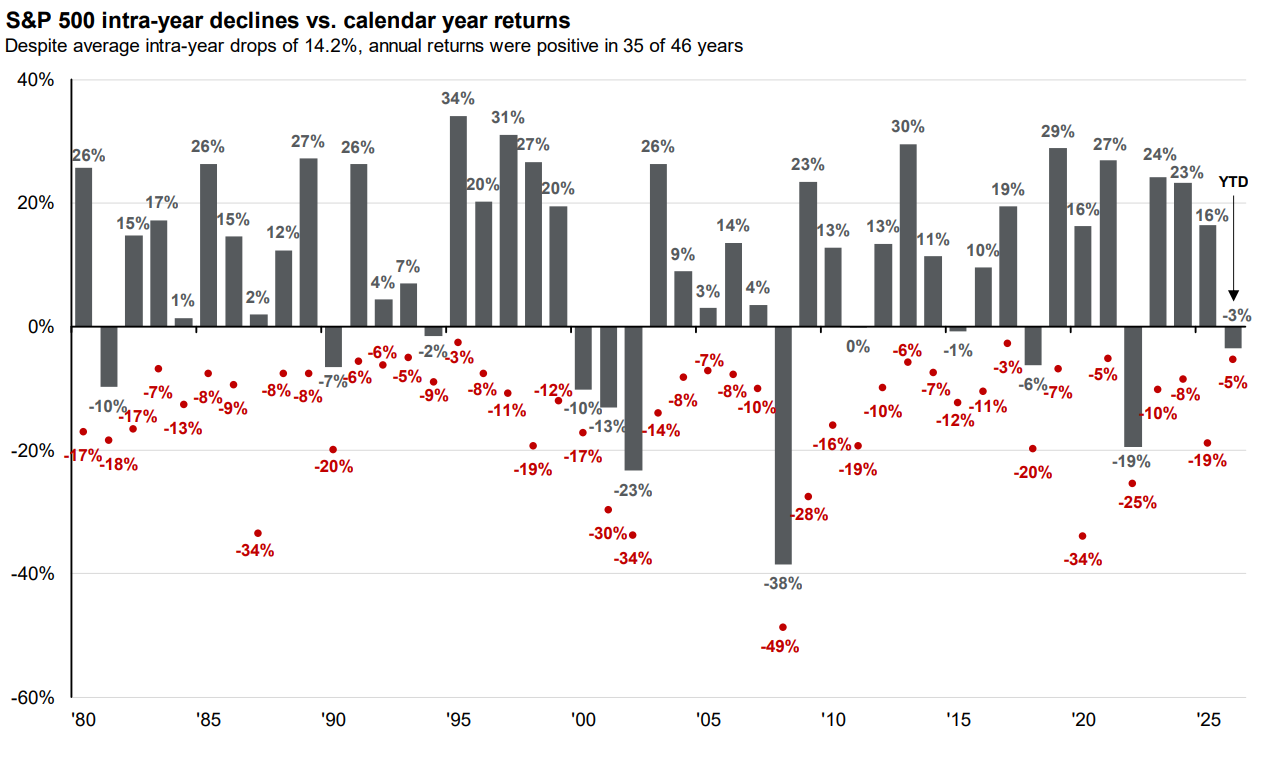

It is important to keep the recent pullback in perspective. The S&P 500 is currently down approximately 7% from its all-time high and about 5% year-to-date—well within the range of normal market volatility. Historically, the average intra-year decline for equities is around 14%.

“While the catalyst has changed—from tariffs to oil—the market’s early-year volatility looks strikingly familiar.”

Chart of The Week

As noted above, the S&P 500 experiences an average peak-to-trough decline of 14.2% in any given year. At present, the market’s drawdown is roughly half that level. Data from JPMorgan, tracking annual declines since 1980, shows that while deeper pullbacks are not uncommon, equities have still delivered positive full-year returns approximately 76% of the time.

Bottom line: short-term market declines are a normal part of investing and do not necessarily dictate full-year outcomes. Last year served as a clear reminder of how quickly sentiment—and returns—can shift.

The commentary in this blog is for informational purposes only and should not be taken as personalized investment advice

Sources: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. Returns are based on price index only and do not include dividends. Intra-year drops refer to the largest peak-to-trough decline during the year. Returns shown are calendar year returns from 1980 to 2025, over which the average annual return was 10.7%. Past performance is no guarantee of future results. Guide to the Markets – U.S. Data are as of March 19, 2026.